Proof is in the Mobile Pudding

The good folks over at CIAJ (Communications and Information Network of Japan) issued a press item last week to announce results of their annual study on cellular phone use. According to CIAJ, “The study aims to capture on-going changes in the domestic mobile communications market and has been conducted since 1998.”

The study includes some interesting results related to actual usage of mobile Internet services, including email, music, GPS, mobile TV, e-wallets, number portability and more. The organization says they mailed questionnaires to 600 cellular phone users (male: 303, female: 297; by age group, under 20: 102, twenties: 101, thirties: 108, forties: 95, fifties: 95, sixties and above: 99) residing in the larger Tokyo and Osaka metropolitan areas from the end of March through April, 2006.

A quick summary of key results:

- 49.2% of those owning handsets with music player functions reported using the function

- 8.2% have used their handsets as an e-wallet; about half planned to use the function in the future

- About half of the respondents have already used or are interested in using ‘1Seg’ mobile TV

- 8.7% said they “would use number portability even if the cost was more than Y2,000”

- Daily use of cell phone features include email (over 80%), downloading ringtones (over 60%), and “camera functions” (approx. 60%)

- 43.3% intend to replace their current handsets

… and the details with my comments.

1. Mobile music

Almost 50% of respondents reported actual use of mobile music, indicating that downloading mobile music is now one of the most popular usages for mobile in Japan. As regards the phone/music player split, 84.3% said that they used their portable music player less so, and their mobile phone more so, to listen to music. In fact, only a small core of 8.3% reported using only a music player, while 7.4% use both devices. CIAJ says the number of phone-only listeners is increasing. In short, these two devices appear to be well on their way to convergence with the phone winning and the portable mp3 player dying.

Note that, outside Japan, even Apple is seeing iPod sales drop, and this survey’s evidence of pending stand-alone mp3 player death in Japan follows on Tomi Ahonen’s analysis of the global situation posted just a few days back on the Wireless-Watch Community site.

2. e-Wallet

While there are no additional details, we can assume this portion of the study refers to FeliCa IC-chip-based phones — the only type of wallet phone in the market and now offered by DoCoMo, KDDI and Vodafone/SoftBank. A mere 8.2% report having used the wallet functions, a tiny usage considering the actual number of enabled handsets sold even by just one carrier (as of November 2005, DoCoMo claimed over 7 mn compatible phones sold). If this is correct, then many mobilers have yet to take FeliCa for a test drive.

But, the other way to look at it, let’s assume that there are probably now some 10 mn FeliCa-enabled phones in mobilers’ pockets (sold by the Big three carriers combined; the true number is probably more like 15 mn). Therefore, an 8.2% actual usage rate means that 820,000 are actually using FeliCa — not bad for the first year of a new technology. Note that the CIAJ study found that about half of respondents plan to use their wallet phone in the future, so carriers’ investment in FeliCa still seems like a good bet. Clearly, phone-based payment usage has a lot of room to grow, and WWJ still thinks 2006 will be the “Year of the FeliCa eWallet Phone.”

3. Mobile TV

“1Seg” is the retail brand for all carriers’ digital mobile TV services. 49.9% responded that they either already use the service (2.3%) or would like to try the service (47.6%). 22.3% responded that they were not sure. Thus 1Seg usage is lower than e-wallet usage, but both enjoy a strong level of popularity if you lend weight to the ‘planned use’ results. With digital mobile TV just coming into the market as this study was conducted (launched on 1 April), we can safely assume that even more are now actually using 1Seg.

4. Number portability

Mobile number portability (MNP) will hit the market later this year, likely by November; the carriers have already published details on how the switching process will work (see the WWJ newsletter from 22 May for our take on the plan), but the final costs have not been published.

In the CIAJ study, 8.7% indicated they would use number portability even if the cost was more than Y2,000. Wow! That’s small and should reassure anyone afraid of massive defections. Further, only a mere 1.4% indicate they would use number portability even if the cost was over Y3,000, while 7.3% said they would if the cost ranged Y2,000 to Y3,000.

The most important factors affecting the decision are: rates (38.2%), same carrier as other family members and friends (23.0%), available services (18.6%), handset design and functions (9.8%) and service area (5.8%). When asked what carrier they would likely be using in one year, 41.9% responded NTT DoCoMo, 27.2% KDDI, 6.4% Vodafone, 0.7% other and 23.8% said they were unsure.

It’s interesting to note that these ratios for desired carrier (i.e. the D41.9, K27.2, V6.4) match closely with the current actual market shares, based on my assessment of TCA numbers for June 2006 (55.64% for DoCoMo, 25.4% for KDDI, 16.41% for Vodafone/SB) and indicate growth for DoCoMo and Vodafone and loss for KDDI. Therefore, WWJ continues to believe that MNP alone will not be the cause of any great defection.

Note that there’s also one further reason — unique to Japan — why MNP is not such a threat: there is no email address portability!

5. Daily usage

Study respondents said that the top three functions used every day on their mobiles are email (over 80%), downloading ringtones (over 60%), and camera functions (approximately 60%). Note: I believe multiple responses were allowed for this question. Interestingly, we’ve also seen surveys that indicate one of the top usages of a mobile is also as a watch and an alarm clock, but few studies seem to bother to ask about this usage.

6. Handset replacement

Of all respondents, 43.3% intend to replace their current handsets, exceeding the 40.6% who do not want to replace current handsets and the 16.1% who are unsure. KDDI has long passed the 85% 3G penetration mark, and DoCoMo caught up to 50% FOMA penetration just a few weeks back. Clearly, a good chunk of the market has been eyeing their friends’ cool new 3G cellies and are thinking about dumping their tired old 2G models. Important considerations for purchasing a replacement are — in order of reported preference — ‘like the design’, ‘can use same phone number’, ‘price’, ‘like the color’, ‘easy to operate’, ‘large screen’, ‘long life battery’, ‘large text for easy viewing and operation’, ‘built-in camera’, and ‘same operation as former model’.

So, what does all this mean?

First, considering Nos. 4 and 6 together, I remain confident in forecasting MNP as only a minor threat. In Question 4, only 8.7% said they’d jump to another carrier at the Y2000 price level, and although 43% in Q6 said they intend to replace their handsets, most of those consider that keeping the same number is one of the top considerations. Thus, if carriers wish to grab a windfall of new subs jumping from a competitor, they are going to have to make defectors a sweet offer and that could be expensive. Clearly, price is also a top consideration in any sort of upgrade, whether within a carrier or moving to another.

Also, it appears that overall mobile data usage has not shifted that much in the past few years.

I recall numerous similar surveys since 1999 in which mail, ringtones and simple surfing were among the top three or four daily usages.

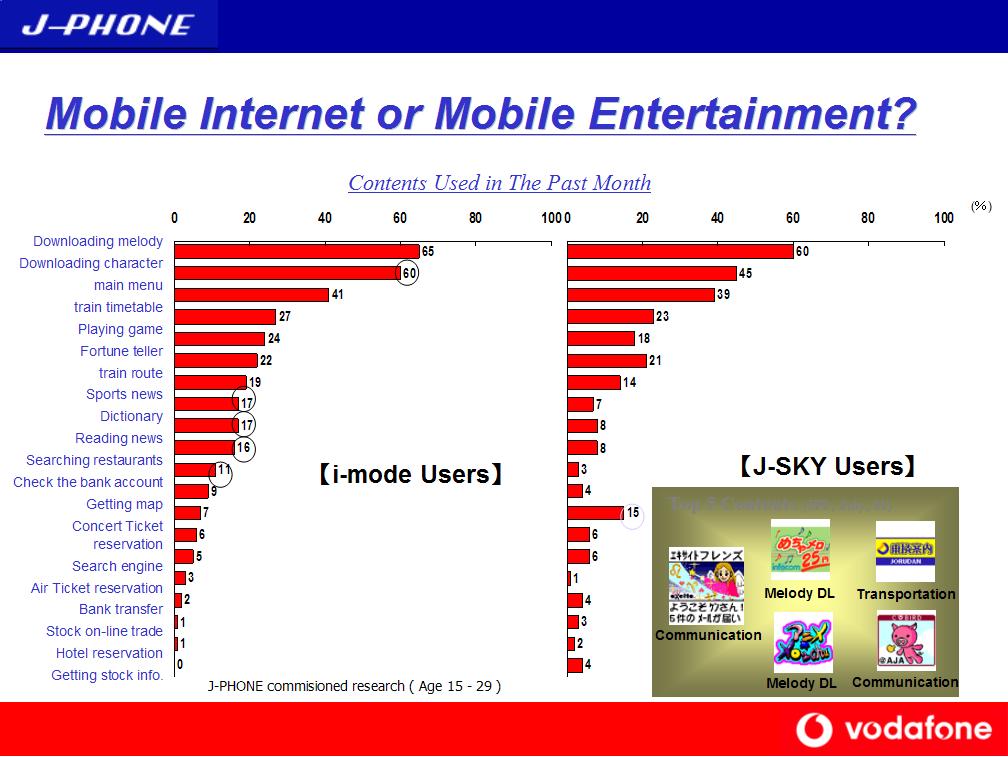

Here’s a screenshot from an old J-Phone presentation from December 2001, showing the top four usages as downloading ringtones & characters, surfing the main menu, and checking train timetables (mail isn’t mentioned explicitly, as this slide only refers to J-Sky Web, but I bet its usage was greater than these):

Here’s a screenshot from an old J-Phone presentation from December 2001, showing the top four usages as downloading ringtones & characters, surfing the main menu, and checking train timetables (mail isn’t mentioned explicitly, as this slide only refers to J-Sky Web, but I bet its usage was greater than these):

Also, I notice in the CIAJ survey that 22.2% of respondents said they used Deco-mail (HTML-format mail), while 35.3% report sending pictures as attachments. These represent rather strong usages for two features that don’t earn the carriers much marginal revenue. This illustrates that, while the presence of useful and popular features may not themselves generate revenue for carriers, these features taken together constitute a rich, complex ‘service-provision system,’ which itself generates large revenues for carriers.

Some of these revenues come in part from taking a small percentage of all IC-chip cash transactions, for example, or licensing access to phone functionality to other large consumer-facing enterprises (for sales and marketing, for example). Thus, additional revenues are created which would not have been possible if only simple phones were provided with mere voice and basic mail functionality.

I also feel even more confident predicting that mobile TV and e-wallet services have nowhere to go but up. While actual usage appears still modest, many users are keen to try these out and will increasingly do so as the ecosystem gets more focused on creating content and advertising just for the small screen, for TV, and deploying more reader/writer point-of-sale terminals, for e-wallet use.

WWJ’s bottom line:

To us, this small survey validates, yet again, the recipe for increasing data ARPU — DoCoMo and KDDI are the world’s leaders — lies in having a very strong and growing value proposition in place flowing from the carrier to the customer, with content providers and tech vendors sharing in the success. An engine only really runs when all cylinders are firing in harmony. Imagine for a moment if only two handsets in a carrier’s fleet of, say, 10 available units, could send/receive SMS. How popular (and therefore profitable) would such a service be? Japan teaches: make services, features and functions a standard, not an option, make them work — easily — for everyone, and give the content owners a good revenue share. And then keep (really) promoting the network and service.

Why is this still so hard for carriers outside Japan to do? Walter Adamson’s recent Op-Ed article serves as an excellent wake up call.

— Daniel Scuka